Better Protection - MediShield Life will provide better protection against large hospital bills and expensive chronic treatments

For All, For Life - All Singaporeans will benefit from MediShield Life protection regardless of health status, throughout our lives

Affordable Premiums - Premiums will go up because of better protection and coverage for all, but Government will provide support to keep premiums affordable

read more

Suggestions on MediShield Life premiums unveiled

The MediShield Life Review Committee (MLRC) has revealed its recommendations on premiums for Singapore’s universal public insurance scheme in its full report released today (June 27).

This follows the committee’s announcement of the recommendations it made to enhance MediShield Life benefits earlier this month.

Although premiums will rise with the enhanced benefits and widened coverage, the committee said that with the premium and transitional subsidies in place, the maximum increase in the first year will be less than S$3 per month for lower- to middle-income Singaporeans and no more than S$6 per month for the higher-income.

read more

Govt to pump in $4 billion to support MediShield Life over five years

The government will pump in around four billion dollars over five years to support MediShield Life, the new national health insurance scheme which will kick in next year.

This is to ensure premium increases remain affordable. Our news desk looks at how much more premiums you would have to pay.

For individuals in the lower-income bracket, those with a monthly per capita household income of $1,100 or less, will get subsidies of between 25 and 50 per cent depending on their age.

NTUC supports MediShield Life recommendations

In a statement, the Labour Movement says it supports MediShield Life, as it will provide all Singaporeans with better protection against large medical bills and assure Singaporeans that they are covered for life.

It says it's reassuring that premiums will be fully covered by Medisave contributions.

NTUC says it's also heartened that the MediShield Life Review Committee has heeded its call to review the potential duplication of medical insurance benefits.

MediShield Life: How much will you pay?

In 2015, with Government subsidies, the maximum increase in premiums will be less than S$3 a month for those in the lower-income bracket, and no more than S$6 a month for everyone else.

The MediShield Life Review Committee released details on the premiums and premium subsidies for the insurance scheme on Friday (June 27). The Ministry of Health simultaneously published an online Premium Calculator to allow Singaporeans to calculate how much they will pay with the new scheme. (MOH website.)

In 2015 - the first year of the insurance scheme, Singapore Citizens will receive a Transitional Subsidy covering 80 per cent of the cost - premiums will range from S$5 a month for those in lower-income households and who are below 20 years old, to S$105 for those above 90 years old living in high-income households. This group would be fully covered under the Pioneer Generation subsidies anyway.

related:

MediShield Life panel details premiums, assures affordability

The MediShield Life Review Committee has revealed, in its final report, details of the increased premiums Singaporeans will have to pay under the Republic’s new mandatory national insurance scheme, with the committee assuring that premiums will be “affordable” with the help of government subsidies.

Younger Singaporeans are set to pay almost three times as much in premiums as they do now, in line with the committee’s recommendations to distribute premiums such that people pay more during their working age and premiums rise less in their old age.

This means a lower-middle-income Singaporean aged 31 to 40 who currently pays S$105 a year for MediShield will pay S$310 a year, before permanent and transitional subsidies to be provided by the Government to the tune of S$4 billion over five years. With the permanent and transitional subsidies, the said person will pay S$134 in the first year of MediShield Life.

related

The Government says it will strengthen the management of healthcare costs in preparation for MediShield Life, since the scheme’s expanded benefits and higher claim limits could lead to over-consumption.

One way it will do so is by stepping up on monitoring claims experience, said Health Minister Gan Kim Yong today (June 28) at the opening ceremony of the Singapore Palliative Care Conference. This monitoring is something that the Government is already doing, where it examines claims that are out of the ordinary to see if the treatment provided is necessary, he said, adding that public hospitals are generally very cost-conscious.

Mr Gan also reiterated that the co-insurance and deductibles included in the public insurance scheme “will encourage our patients to make informed decisions, to make wise decisions, with regards to their care needs”.

related:

Higher Medisave withdrawals for palliative care

Palliative care services for the sick and dying will be ramped up significantly over the next six years as Singapore's population ages.

There will be more hospice beds, home palliative care services and a new graduate diploma course to train more doctors.

People will also be allowed to use more of their Medisave money for these services, with no withdrawal cap for those who are terminally ill.

read more

MediShield Life subsidies can be further enhanced: Chia Shi-Lu

The head of the Government Parliamentary Committee (GPC) for Health, Dr Chia Shi-Lu, has welcomed the premiums that were recently announced for MediShield Life, saying they were lower than what some had expected.

But Dr Chia said subsidies can be further enhanced for other vulnerable groups of people.

He said the initial feedback gathered is that the premiums are at a reasonable amount.

related: MediShield Life Review committee: how to make IPs work better

read more

The MediShield Life Conundrum

Singaporeans may realise that the biggest joke currently in vogue in town is the MediShield Life. Since its introduction with the massive efforts by PAP minister, including the inimitable PM Lee Hsien Loong, to explain the so-called panacea to help especially finance-strapped Singaporeans, particularly the impecunious elderly, to defray their hugh medical bills, the cynical joke is that very few people, especially the elderly, understand the intricacies of the over-hyped scheme. They could only apprehend with certain amount of incredibility what government leaders have told them of the benefits they they would get out of MediShield Life but how they would benefit, whether financially or medically, is all Greek to them.

The smart Alec minister or ministers who so ingeniously compiled the MediShield Life scheme should be congratulated for his ingenuity in devising such an intricate scheme that has almost every rational Singaporean, young and old, baffled. It will be some kind of miracle if government leaders could ultimately unravel this so-called humanitarian puzzle to the benefit of Singaporeans, especially the elderly.

One wonders where the problem lies. Is it because government leaders have not found the knack of explaining the scheme in a language the would-be beneficiaries would find it easy to understand? Or is it because the would-be beneficiaries are so obtuse that no amount of explanation, however simple, would be comprehensible to them? Anyway, this seems to be a million-dollar question which behoves the PAP leadership to find a quick solution.

read more

HEALTH MINISTER GAN KIM YONG: I CANNOT ASSURE S'POREANS THAT MEDISHIELD PREMIUMS WON'T INCREASE AFTER 5 YRS

MediShield Life premiums will remain the same for the first five years, said Minister for Health Gan Kim Yong.

The assurance on the new universal health insurance scheme was given by Mr Gan on Saturday, a day after the MediShield Life Review Committee unveiled its recommendations.

He also said the standardised Integrated Shield Plan for Class B1 wards will likely start along with MediShield Life at the end of 2015.

read more

Medishield Life: ‘Premiums will need to increase’

The Government announced today (27 Jun) that it has accepted all the recommendations of the MediShield Life Review Committee (MLRC) with regard to the MediShield Life scheme. It said it will provide close to $4 billion in subsidies and other forms of financial support over the next five years.

“With better benefits, premiums will need to increase, but will be able to be fully paid for from Medisave. The Ministry of Health will ensure that Medisave Withdrawal Limits can continue to fully cover MediShield Life premiums, and the additional 1%-point Employer’s Medisave contribution from 2015 will also be sufficient to cover the increases in MediShield Life premiums for most households,” MOH said.

MOH said support will be in the following forms:

- Government bearing the bulk of the cost of bringing those who have pre-existing conditions into MediShield Life. Government will pay for three-quarters of the cost in the first five years (about $850 million over five years). This will ease the shift to universal coverage under MediShield Life and keep the premium impact manageable for all;

- Premium subsidies i.e. Pioneer Generation subsidies and subsidies for lower- to middle-income Singaporeans, and Additional Premium Support on a case-by-case basis for the needy (about $430 million per year). These will remain permanent features of MediShield Life; and

- Transitional subsidies (for all Singapore Citizens) for the first four years (about $830 million over four years).

Medishield Life Bites Hard

At its core, universal health coverage (UHC) is about giving the individual and his family access to health care and preventing them from facing financial ruin that can come from unexpected illness and disability. At least that was what Prussian chancellor Otto von Bismarck, widely credited as the intellectual father of today's UHC programmes, had in mind when he introduced national compulsory coverage for workers. Profit was never the motive.

Last year, Medishield premiums were quietly increased without much fanfare. Han Fook Kwang himself woke up to discover that his MediShield premium had jumped to $1,589, double what was deducted ($800) from his Medisave account previously. Before you could even contemplate bailing out of the scam, they introduced the compulsory Medishield Life to skim you off for perpetuity.

For a while now, the spiel was about additional benefits, never about whether we need them or are prepared to pay for the extras. They can hide the numbers only for so long. Now the secret is out.

read more

Medishield Life - Monthly Premiums (2019)

read more

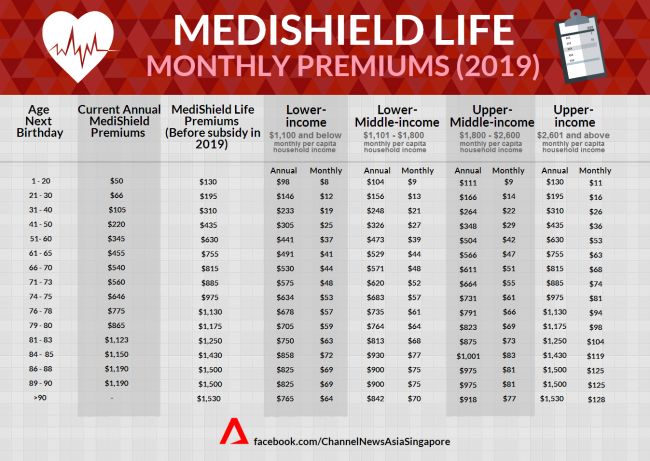

Medishield Life - Monthly Premiums (2019)

According to a table presented by Channel News Asia titled, Medishield Life – Monthly Premiums (2019), Singaporeans are classified under four categories by income. These are Low Income for those earning $1,100 and below, Lower Middle Income, $1,101 to $1,800, Upper Middle Income, $1,801 to $2,600 and Upper Income for those earning above $2,600

The table is based on per capita income and very likely to assume that each household has two working adults or two incomes. It is very generous and a compliment to claim a household income of $5,200 as belonging to Upper Middle Income. At $5,200, many are struggling to own a car or to live comfortably if they have two school going children, and hopefully don’t have parents to look after. For a household with only one income, a $2,000 household income is barely above subsistence level or just above the poverty line for a family of four.

To make the classification less realistic, put them in comparative terms like poor, average, rich and very rich. I don’t think anyone will agree that a household income of $3,600 to $5,200 can be considered as rich. So is a household income of more than $5,200 as very rich, Upper Class. Ok, Upper Income is not necessarily upper class.

read more

read more

Snapshot: Medishield Life premiums can be changed anytime by the government depending on medical inflation and claims experience

Straits Times, 27 Jun 2014

Straits Times, 27 Jun 2014

Comment: From past experience, promises made before the General Election have no bearing on what comes after the poll.

read more

read more

MEDISHIELD LIFE: PREMIUMS INCREASE YEARLY TO AS MUCH AS 189% BY 2019?

We refer to the article “MediShield Life review: Premium increase much lower than feared”

Increase in premiums mostly absorbed by subsidies and top-ups? It states that “The increase in premiums which people will have to pay for the better benefits under MediShield Life will not be more than $355 a year, with most of it absorbed by various government subsidies and top-ups.”

111 to 189% increase in premiums? - The increase in premiums from 2019 compared to the current premiums, after the declining transitional subsidies range from 111% (from $9 to $19 monthly for the lower-income with household per capita income less than $1,100) to 189% (from $9 to $26 for the high income) for age 31 – 40. For age 51 – 60, the increase range from 28% (from $29 to $37 for the lower-income) to 83% (from $29 to $53 for the high income).

So, how can an increase of up to 111% for the lower-income, and up to 189% for the higher income, be arguably called a “premium increase much lower than feared”?

related:Medishield Life – huge premium increase will be an issue

MediShield Life: Automatically on “household per capita income”?

Affordable MediShield Life?

read more

So, how can an increase of up to 111% for the lower-income, and up to 189% for the higher income, be arguably called a “premium increase much lower than feared”?

related:Medishield Life – huge premium increase will be an issue

MediShield Life: Automatically on “household per capita income”?

Affordable MediShield Life?

read more

MediShield Life Review: Better coverage for all, enhanced benefits, lower co-payments

The MediShield Life Review Committee has come up with recommendations for the compulsory insurance plan that aim to ease people's worries about racking up large hospital bills.

In considering changes to MediShield Life, the Committee had "carefully considered the balance between the impact of the benefit enhancements and the resulting indicative premium levels", it said in a release on Thursday. The Committee recommended the following:

The MediShield Life Review Committee has come up with recommendations for the compulsory insurance plan that aim to ease people's worries about racking up large hospital bills.

In considering changes to MediShield Life, the Committee had "carefully considered the balance between the impact of the benefit enhancements and the resulting indicative premium levels", it said in a release on Thursday. The Committee recommended the following:

- remove the lifetime claim limit of $300,000;

- increase the policy year claim limit from $70,000 to $100,000

- increase the daily claim limits for normal wards and ICU wards by up to 55 per cent

- increase the claim limits for surgical procedures by between 25 and 93 per cent

- increase the daily claim limits for community hospitals by 40 per cent from $250 to $350

- increase claim limits for outpatient cancer chemotherapy and radiotherapy to better cover the cost of subsidised cancer treatment

- lower the co-insurance rates from the current range of 10 to 20 per cent to 3 to 10 per cent, and

- start premium rebates earlier from the age of 66, instead of 71.

With MediShield Life, the current age limit of 90 will be lifted so Singaporeans can enjoy life-long coverage. Those with pre-existing conditions will also be covered.

read more

read more

MediShield Life: Premium increase to range between 111% to 189% for the “young”

We refer to the article “MediShield Life review: Premium increase much lower than feared” (Straits Times, Jun 27) .Increase in premiums mostly absorbed by subsidies and top-ups?

The ST article writes that based on the report released by the MediShield Life Review Committee, the increase in premiums which people will have to pay for the better benefits under MediShield Life will not be more than $355 a year, with most of it absorbed by various government subsidies and top-ups.

However it is alarming to note that the increase in premiums from 2019 compared to the current premiums, after the declining transitional subsidies, range from 111% (from $9 to $19 monthly for the lower-income with household per capita income less than $1,100) to 189% (from $9 to $26 for the high income) for age 31 – 40.

read more

read more

BEWARE OF PRIVATE INSURERS PROFITEERING FROM NEW MEDISHIELD LIFE HEALTH INSURANCE

SINGAPOREANS should welcome MediShield Life, the updated universal health insurance plan being designed. It improves on the current Central Provident Fund (CPF) MediShield scheme by providing lower out-of-pocket medical expenses due to reduced co-payment rates. There are also higher benefits, higher annual claim limits, and an unlimited lifetime limit. There is even an extension of cover from the current maximum 90 years of age to lifetime.

SINGAPOREANS should welcome MediShield Life, the updated universal health insurance plan being designed. It improves on the current Central Provident Fund (CPF) MediShield scheme by providing lower out-of-pocket medical expenses due to reduced co-payment rates. There are also higher benefits, higher annual claim limits, and an unlimited lifetime limit. There is even an extension of cover from the current maximum 90 years of age to lifetime.

In addition, those who opted out previously or have been excluded due to pre-existing conditions will be included in MediShield Life. But as a finance professional, I have some longer-term policy concerns.

In my view, the Government should consider a more sustainable universal health insurance model where risks are pooled even more, in order to avoid "cherry-picking". Cherry picking occurs when private insurers take on healthy individuals and leave the remainder in the underlying CPF MediShield pool.

read more

read more

MEDISHIELD LIFE COULD SEE YOU PAYING UP TO DOUBLE THE CURRENT MEDISHIELD PREMIUM

MediShield Life – everything also increase?

We refer to the article “Enhanced benefits proposed for MediShield Life” (Today, Jun 6).

The following questions remain unanswered: Medishield scheme accumulated surpluses? What is the accumulated surplus plus interest since the MediShield scheme has had annual surpluses since its inception? About $1 trillion? Still not spending any money on healthcare?

From a cashflow perspective, will the Government still not be spending a single cent on healthcare because Medisave contributions in a year may continue to exceed all withdrawals including government healthcare spending? Are there any countries in the world that operate their healthcare system like this?

read more

read more

Snapshot: Singapore Government classifies income above $2600 as "Upper Income" in Medishield Life Premium Tabulation

Hardwarezone Forum, 27 Jun 2014

read more

It Is Time The Government Is Transparent To Singaporeans On Healthcare Costs

Singaporeans have to pay our CPF into the Medisave for health. We then have to pay our Medisave into Medishield, also for health.

When we have to take our Medisave to pay for Medishield, doesn’t that means we have less money to use in the Medisave?

Also, if we are already paying into so many schemes – tax, Medisave, Medishield and Medifund (as well as ElderShield etc), why is it still not enough to cover for our healthcare expenses, that we still have to buy private Medishield plans, accident plans etc from private insurers?

read more

Singapore Daily

– Healthcare From Spore and Beyond: Medishield Life: Immediate Reactions

– Inve$tment Moat$: My tots: Medishield Life, Private Plans & Worries as a Single

– Bertha Harian: Medicating Medishield for life

– My Singapore News: Medishield Life – Monthly Premiums (2019)

– Living Investment: Feeling left out in Gov subsidies – Medishield Life Premium

– Singapore Recalcitrant: The MediShield Life Conundrum

– Singapore Notes: Medishield Life Bites Hard

– The Heart Truths: It Is Time Gov Is Transparent To Spore On Healthcare Costs

– Five Stars and a Moon: CPF: My money is my money?

– SingaporeNew Policy Thinking: Redesigning CPF, stripping it down to the basics

read more